Despite being better educated, Millennials are earning less and struggling financially

Millennials are facing a significant financial shortfall compared to previous generations, earning 20% less than baby boomers did at the same age. This stark reality is outlined in The Emerging Millennial Wealth Gap, a recent report by the nonpartisan think tank New America. The median earnings of millennials (ages 18 to 34) today are lower than those of their counterparts in the 1980s, with the pay gap first noted in a 2017 report by Young Invincibles. This gap persists despite an increase in education levels.

Nearly 40% of millennials aged 25 to 37 hold at least a bachelor’s degree, compared to just a quarter of baby boomers and 30% of Gen X at the same age, according to Pew Research Center

However, this increase in educational attainment has not translated into higher earnings for the generation. Instead, millennials face unpredictable paychecks, with many working in contract and freelance positions that offer less stability in hours and compensation.

The lower wages millennials are earning have long-term consequences for their ability to build wealth. Reid Cramer, director of New America’s Millennials Initiative, argues that millennials are on a “completely lower trajectory” compared to previous generations. According to the report, millennials’ wealth in 2016 (ages 23 to 38) was 41% lower than that of those in the same age group in 1989, highlighting a growing generational wealth gap.

For young families, the wealth gap is equally concerning. In 2016, households headed by individuals under 35 had an average net worth of just $10,900, a significant drop from $18,900 in 1995. This drop reflects the broader financial struggles millennials face, particularly the challenges posed by the Great Recession and its aftereffects.

The recession, which began in 2007, had a lasting impact on millennials, especially those who entered the workforce during or after the economic downturn. With fewer job opportunities and lower wages, millennials started off at a significant disadvantage compared to previous generations. At the same time, many were burdened with higher education costs, resulting in greater student loan debt and personal financial struggles.

The recovery from the recession, while steady, was uneven. As Cramer notes, well-off households fared better during the recovery, with wealthier individuals benefiting from the rebounding economy at the expense of others. In 2016, the top 10% of income earners in the U.S. received half of the nation’s total income, a sharp increase from 38% in 1992. This trend further exacerbates the financial divide between the wealthiest and the rest of the population.

Millennials’ financial struggles are not just reflected in their income, but also in their ability to achieve traditional milestones. Marriage rates among millennials are projected to drop by 70%, with many delaying or opting out of marriage altogether. The Urban Institute estimates that a record number of millennials will remain unmarried by age 40. This delay in life milestones is directly tied to the financial instability many millennials face.

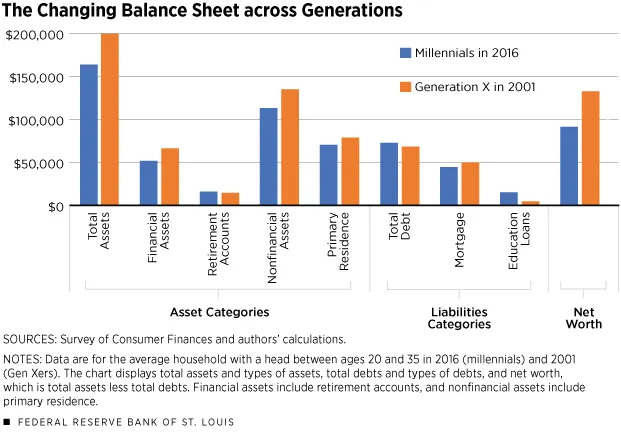

Homeownership, once considered a key avenue for building wealth, is also increasingly out of reach for millennials. The average millennial held $162,000 in assets by 2016, compared to $198,000 for Gen X at the same age, according to the St. Louis Federal Reserve. The volatility in income, combined with higher living costs, has made it harder for millennials to invest in real estate, which has historically been a primary means of accumulating wealth.

This financial instability also has broader implications for future generations. Liz Hipple, senior policy advisor at the Washington Center for Equitable Growth, argues that millennials’ struggles could have negative consequences for their children. With fewer resources available to invest in their children’s education and health, the potential earning capacity of future generations may be limited, creating a cycle of financial hardship.

Cramer warns that this generational wealth gap could have a profound effect not only on millennials but on the entire economy. Millennials’ inability to build wealth, retire comfortably, or pass on assets to the next generation could strain social systems and perpetuate inequality. The lower pay, volatile income, and reduced wealth accumulation may create lasting challenges, not just for millennials, but for society as a whole.